Car parking market

Parking is an indirect service, necessary to provide access to businesses and regions and for the mobility of people. In situations where demand is high (many people at the same time) and supply is low (limited space) the need for regulation arises along with setting an economic value of parking spaces. An additional requirement is the quality of the public space, which also has an impact on the value of the property and amenities in the surrounding area.

The desire in inner-city areas to park cars ‘out of sight’ where they take up a limited amount of space results in the need for purpose-built parking facilities. This can offer visitors greater comfort (directions, short walking distances) and safety. Research shows that visitors to city areas are willing to pay for parking at a short walking distance from their destination.

The car parking market's quantitative approach is based on research and reports from various countries, from statistics organisations (such as Statistics Netherlands (CBS), INSEE, DESTAT) as well as from research institutions in the field of mobility and urban development (such as RAC and CERTU).

Number of parking spaces in Europe:

The availability of parking spaces can be divided into five main categories:

- Parking at home or at work on private property, not accessible to third parties.

- Public on-street parking.

- Public parking in car parks, with barriers if required.

- Public and semi-public parking at shops and offices.

- Public parking in purpose-built facilities.

The total number of parking spaces in the 28 EU countries is estimated to be 440 million, approximately two spaces for every passenger car. Of these, some 40 million parking spaces are regulated in one way or another:

- Approximately one-third by permits issued by municipalities.

- Approximately one-third by paid street parking operated by municipalities.

- Approximately one-third in parking facilities operated by private parties.

Mobility and parking:

Each car makes an average of 2½ traffic movements every day. We can distinguish four main groups:

- commuting,

- shopping,

- social and leisure,

- business travel.

Each car travels for an average of one hour per day, is parked near the home for sixteen hours and elsewhere for seven hours per day. Of these seven hours, the majority is at work, about 45 minutes at the shops and more than an hour at social and recreational venues.

There is some stagnation in the development of car usage among young adults aged between 18 and 29 years, due to the decrease in the number of young adults in employment and due to the increase in students living in urban areas. Among this group, the status of owning a car is also changing. On top of all this, we have the sobering effect of the economic crisis on car use. In the coming years, under the influence of an improving economy, car usage is expected to increase by an average of 1½% per annum.

The sharp rise in the opportunities presented by ICT and its use in society are having the opposite effect on mobility. On balance, the influence of ICT on total mobility is limited. The number of people teleworking has increased, particularly among the higher educated, however, the time spent commuting did not visibly decrease. After all, many people telework only for a portion of the working day. In addition, online shopping has increased greatly in volume and for some people, this means reduced mobility, while for others it leads to extra mobility (visiting webshops makes people curious and ultimately leads to visiting actual shops further away).

Free parking and paid parking:

The vast majority of parking is not paid directly by the user. Parking near the home is often perceived as free, even though the cost is included in the costs of the home or paid periodically in the form of a permit. At the place of work, parking is almost always paid by the employer. At shops, approximately 8% of parking has to be paid for directly. In all other cases, the parking facilities are financed by the municipality (from public funds), a shopping centre (through a surcharge in the retail rent), or similar body.

Parking tariffs for visitors vary from EUR 0.50 per hour to EUR 1.00 for 10 to 12 minutes at the most popular locations in large cities.

As a result of free parking or parking below cost price with permits, paid parking comes nowhere near to covering the costs. Various studies indicate that only a quarter of the total cost of parking is paid directly by the users and the majority is paid by others, such as taxpayers. In this way, cyclists and users of public transport contribute to the cost of ‘free’ parking.

Part of the paid car parking market is unused due to insufficient monitoring of payment compliance. With barriers at car parks and off-street parking areas payment is more or less assured. On-street parking has to be monitored and enforced with fines or additional fees. In some countries (Germany and France, for example) the penalty for not paying and the chance of being caught are so low that only one in five users actually pays, which means that some 80% of the relevant market segment goes untapped. This creates differences between figures for parking revenue realised and the parking market.

The car parking market in the 28 EU countries is calculated to be worth EUR 40 to 45 billion. The actual revenue from parking is calculated by the European Parking Association (EPA) at slightly more than EUR 29 billion, but this is excluding VAT where applicable, reservation costs, earnings from Parking Service Providers and the like.

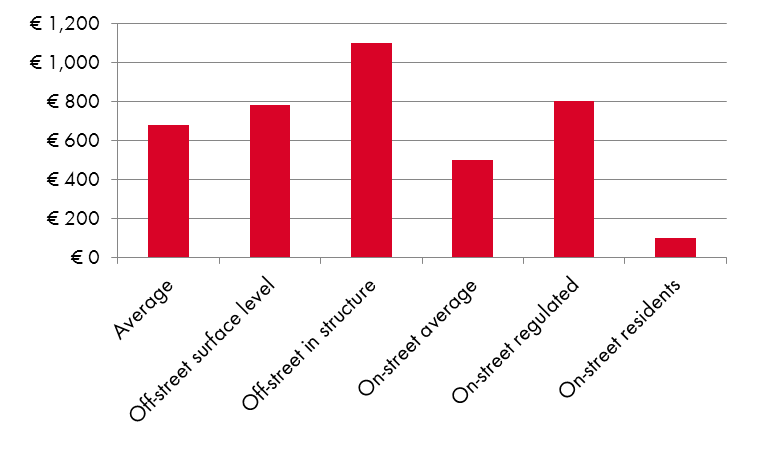

EPA calculation of average revenue per annum:

- The average revenue per space is EUR 679.

- For off-street surface level, EUR 780.

- For off-street in structure, EUR 1,100.

- For an on-street space, EUR 496:

- EUR 800 for public spaces,

- EUR 100 for residents.

Average revenue per parking space, 2013, EPA

Q-Park in the car parking market

Q-Park operates in ten countries, which represent 53% of the European population and 69% of the Gross Domestic Product (GDP) of the EU. The GDP per inhabitant in the ten Q-Park countries is twice as high as that in the other EU countries. Car usage and thus parking is closely linked to the development of the GDP.

In the ten countries where Q-Park operates, Q-Park has a total share of approximately 2½% of the total car parking market. In the Netherlands, Q-Park's share of the total car parking market is some 12%.

The car parking market as a whole is highly fragmented: the five major international parking companies operate approximately 6% of the total car parking market in the 28 EU countries. Other players include:

- local authorities or parking companies owned by the municipality

- small local private parking companies

- railway companies with their own parking companies for P+R

- hospitals, shopping centres and airports that manage their own parking facilities.

Parking tariffs

Basically, parking tariffs depend on demand: the number of visitors who come by car and who want to park in the same place at the same time. On the other hand, the parking tariff is determined by the number of available parking spaces. Parking tariffs differ from country to country.

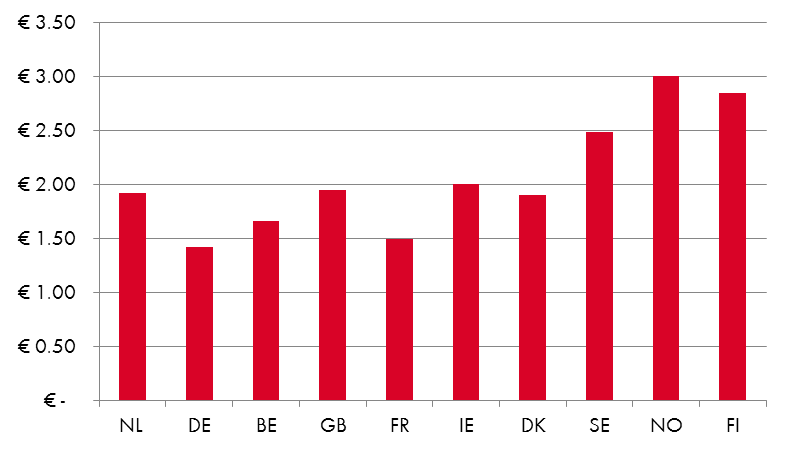

Q-Park average parking tariff per hour, per country

In Germany and France the average parking tariff is 25% respectively 22% below the average of the ten Q-Park countries, while the average tariff in Norway and Finland is 60% and 50% higher, respectively. In the Netherlands, the tariff is more or less at the average level.

In economically good times with significant inflation it is customary that parking tariffs increase by 1 or 2% above the rate of inflation. In 2013 there was hardly any inflation and we noticed that tariff increases were under considerable pressure. As a result, discussions about paying by the minute increased, following the example of Spain, where parking by the minute has been customary since a change in legislation in 2007.

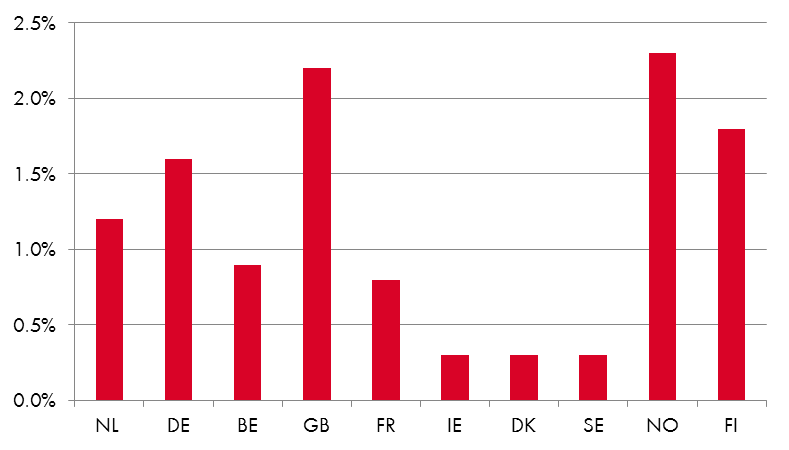

Annual inflation

Parking as sub-service

One threat to the car parking market is that service providers are increasingly including parking in their comprehensive range of services. These service providers collect the total amount from the customer and then, after deducting a percentage as a commission, pay the operator for the use of the parking space. Through identification by means of the owner's smartphone or the vehicle number plate, these service providers can monitor the parking behaviour of customers closely and therefore offer customised services.

Competition

Customers theoretically have the choice between parking in car parks, on the street or elsewhere in the public space. This may be as close as possible to the destination or at some distance, for example, in a P+R facility. New developments, such as paying for on-street parking with a mobile phone make parking ‘outside’ more attractive and are shifting the competitive relationship.

There are considerable differences between the private parties who are active within the parking industry: from small local businesses with just a few facilities in a single city to the large companies operating internationally, such as Q-Park. The latter group does not dominate in volume. Currently, the top five companies operating internationally manage and operate only about 6% of the total regulated car parking market.

In 2013, the EU tightened up legislation governing competition for those local authorities who manage and operate parking in the public space as well as in purpose-built facilities, with the Public Enterprises (Market Activities) Act. They must implement the legislation in the course of 2014. The aim is to maintain the ‘level playing field’ in the industry. This will have a positive influence on the position of private companies such as Q-Park.